How to improve acceptance rates without adding friction

Approval rates are one of the clearest signals of payments performance, but they’re really a business metric.

A small improvement in successful transactions can lift conversion, improve customer acquisition efficiency, reduce involuntary churn, and make revenue more predictable. That’s why approval performance matters so much for digital businesses, especially those with recurring billing or high transaction volumes.

The challenge is that declines are often treated as a part of operating online. In reality, many are preventable.

Why payments get declined

Not all declines happen for the same reason.

Some come down to simple customer input errors, like mistyped card details or expired cards. Others are caused by fraud settings that are too aggressive, risk decisions by the card issuer, or stored payment credentials that are no longer current.

That matters because approval rates rarely improve from one fix alone. They improve when businesses understand where friction sits across the payment journey and start tuning the right parts of the system.

The levers that influence acceptance performance

There are several ways to improve acceptance rates, and the best results usually come from using more than one.

Checkout experience

Clean UX, fewer unnecessary fields, strong mobile design, clear error handling, and wallet support all reduce input mistakes and abandonment before authorisation even begins.

Fraud tuning

Fraud controls need to block bad transactions without blocking legitimate customers. Teams that review fraud rule performance regularly tend to reduce false declines and protect more revenue.

Stored credentials and returning customers

Pre-filled details, secure credential storage, and a low-friction repeat purchase flow help reduce avoidable failures for returning customers.

Send the right transaction type indicators

Flagging recurring, instalment, or merchant-initiated transactions (MIT) correctly helps card issuers apply the right risk model. Mislabelled MITs are a common source of unnecessary declines.

Retries and dunning

In recurring payments, well-timed retries and clear customer communication can recover revenue that would otherwise be lost to temporary or soft declines.

All of these matter. But there’s another lever that often gets less attention than it should: the quality of the credential being submitted.

The overlooked lever: credential quality

Many businesses spend time improving what happens around the transaction, without looking closely at the payment credential itself.

That can be a blind spot.

When a stored card is static, exposed across multiple systems, or no longer up to date, issuers have less confidence in the transaction. That can increase defensive declines, especially in digital and recurring environments.

Improving credential quality helps shift that starting point. One of the clearest ways to do that is through network tokenisation.

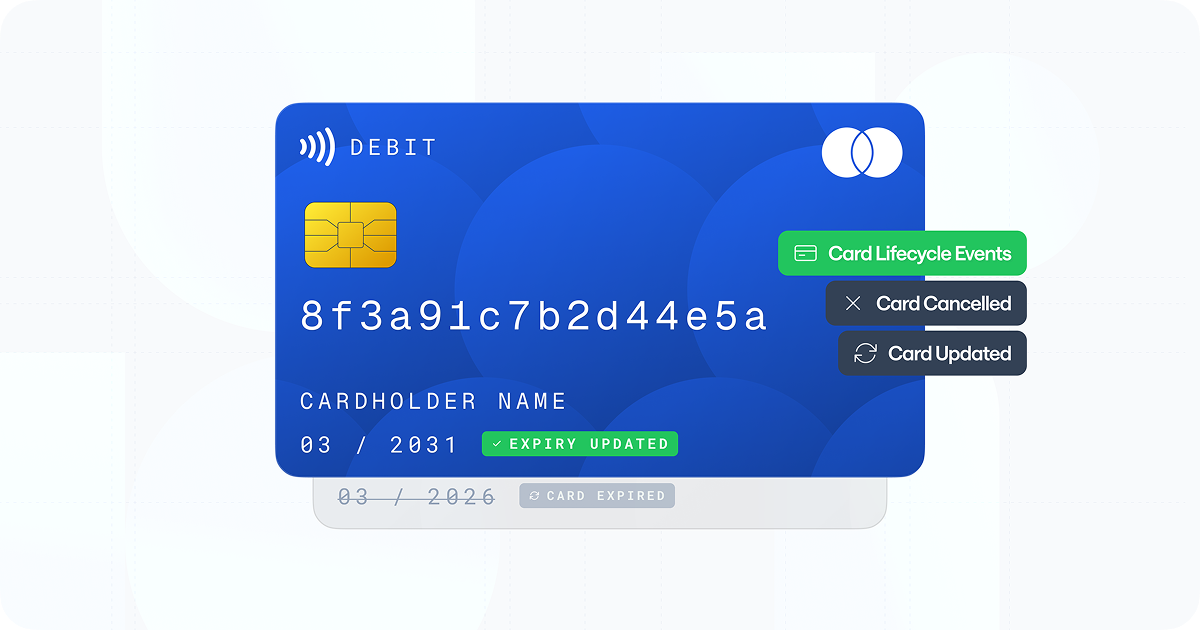

Where network tokens fit

Network tokens are scheme-issued payment credentials from providers like Visa, Mastercard, and Amex. They replace the raw card number with a tokenised credential linked to a specific merchant, PSP, or wallet.

That brings a few important advantages.

They can improve credential security, provide stronger trust signals to issuers, and support lifecycle updates when cards expire or are reissued. In recurring payments, that can reduce failed renewals and help protect revenue that might otherwise be lost to stale card data.

That doesn’t make network tokens a silver bullet. But it does make them a valuable part of a broader approval strategy.

Approval optimisation is a systems problem

The most effective approach to approval rates is usually layered.

Better checkout reduces input errors. Better fraud settings reduce false positives. Better retry logic recovers temporary failures. Better credentials improve issuer confidence.

Network tokens strengthen that system. They don’t replace the surrounding work, but they can make the rest of the stack perform better.

That’s often the difference between treating declines as inevitable and treating approval performance as something you can actively improve.

Final thought

If approval rates are under pressure, it’s worth looking beyond a single metric or feature.

The real opportunity is to understand the full payments system around the transaction, then improve the parts that have the biggest commercial impact. Sometimes that means better UX. Sometimes it means tighter fraud tuning. Sometimes it means rethinking the credential itself.

Network tokens are one of the tools that can help, particularly for businesses focused on recurring revenue, digital conversion, and long-term payment performance.